You borrowed a friend's car, had an accident, and weren't listed on their policy. Now you're facing suspension, SR-22 requirements, and liability claims you didn't expect. Here's what happens next and how to protect your license.

Why a Borrowed-Car Accident Triggers Uninsured-Driver Suspension

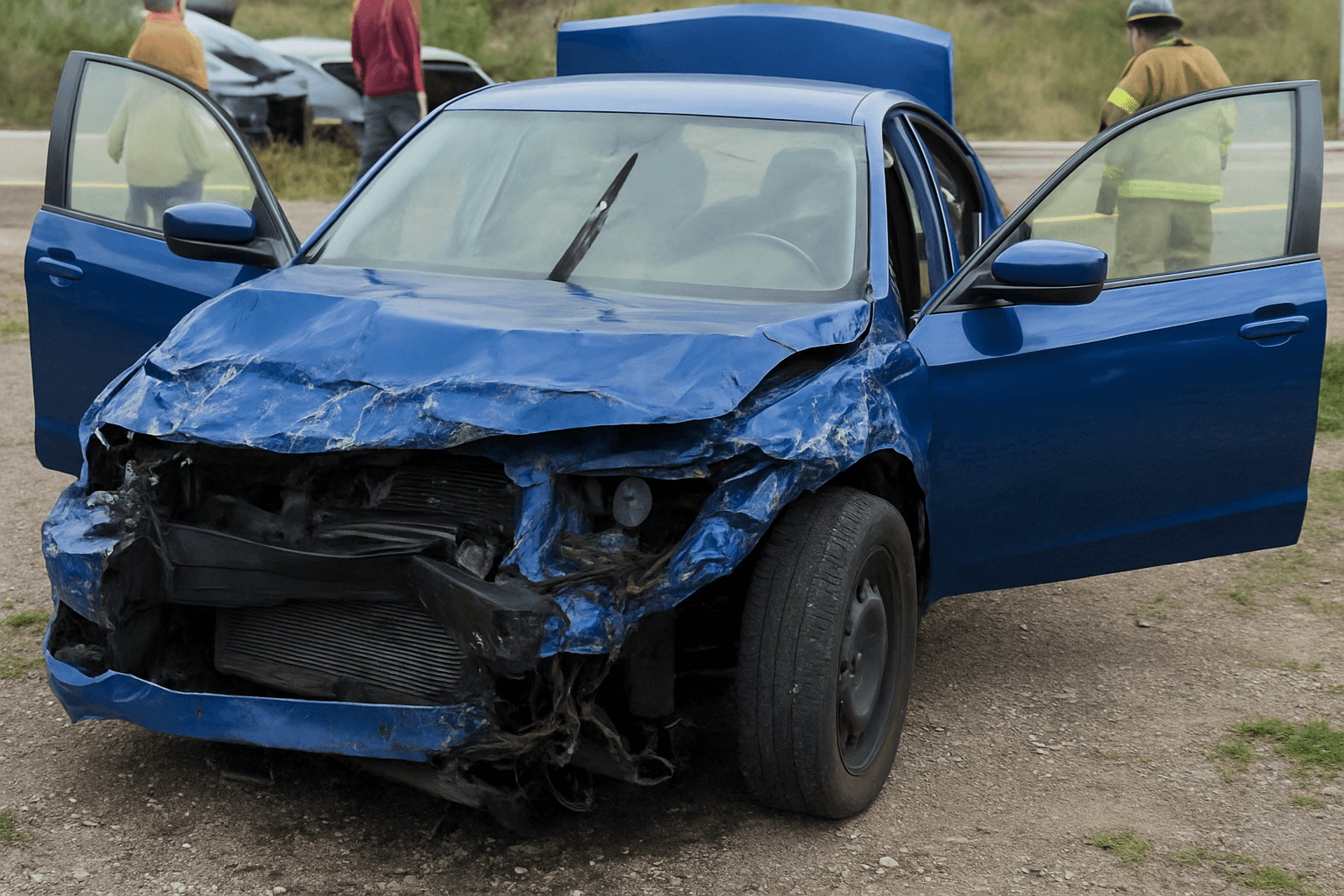

The accident happened in a borrowed car, and the owner's insurance denied your claim because you weren't listed as a permissive driver. Most states treat this scenario as uninsured driving, triggering suspension even though you weren't driving your own vehicle. The DMV doesn't distinguish between owning an uninsured car and operating someone else's uninsured vehicle—both create financial responsibility violations.

Your license suspension starts when the accident report reaches the state DMV, typically 10 to 30 days after the crash. Some states issue an immediate administrative suspension notice if the responding officer documents no valid insurance at the scene. You'll receive a suspension notice by mail listing the violation date, effective suspension date, and reinstatement requirements—usually SR-22 filing, proof of financial responsibility, and a reinstatement fee.

The borrowed-car element complicates liability. If the owner's policy covers permissive use and you were driving with permission, their liability coverage should respond first. But if you're excluded from their policy, weren't given permission, or the owner lied about permissive use to avoid a claim, their carrier denies the claim and the state treats you as the uninsured party. You're now liable for property damage, bodily injury, and your own suspension consequences.

Dual Liability Exposure: The Accident Claim and Your Suspension

You face two separate legal consequences. The first is civil liability for damages—property damage to the other vehicle, medical bills if anyone was injured, and possibly the owner's vehicle damage if their policy didn't cover it. The second is your license suspension for driving uninsured. These run on parallel tracks with different timelines and different agencies.

The accident claim doesn't disappear when your license suspends. The other driver's insurance company will pursue you directly if their insured has collision coverage and they paid the claim under subrogation. If the other driver was uninsured or underinsured, they may sue you personally. Settlement demand letters typically arrive 30 to 90 days after the accident. Ignoring them leads to civil judgments, wage garnishment, and in some states, extended license suspension until the judgment is satisfied.

Your suspension proceeds separately. The DMV suspends your license for the uninsured-driving violation regardless of whether the accident claim settles. Reinstatement requires SR-22 filing, proof you've secured liability insurance meeting state minimums, and payment of reinstatement fees. Most states require 1 to 3 years of continuous SR-22 coverage after a no-insurance accident. If you let the policy lapse during that period, the clock resets and your license suspends again.

Compare car insurance rates in your state

Get quotes from licensed carriers — no obligation, no spam, results in minutes.

Get Your Free Quote✓ No Obligation Required✓ Licensed Carriers Only✓ Available Nationwide✓ Free to Compare

SR-22 Filing After a Borrowed-Car Accident: Do You Need to Own a Vehicle?

You don't need to own a vehicle to file SR-22. If you sold your car, never owned one, or the borrowed vehicle was impounded or totaled, a non-owner SR-22 policy satisfies the state's filing requirement. Non-owner policies provide liability coverage when you drive a vehicle you don't own—exactly the scenario that caused your suspension.

Non-owner SR-22 costs less than standard SR-22 because it doesn't cover a specific vehicle. Monthly premiums typically range $40 to $90 depending on state minimums, your age, and the accident severity. The SR-22 filing fee itself runs $15 to $50, paid once when the carrier submits the certificate to your state DMV. The policy must remain active for the entire filing period—1 to 3 years in most states, 5 years for repeat violations in some jurisdictions.

If you plan to borrow cars regularly or use rideshare vehicles, non-owner SR-22 protects you during the filing period. If you buy a vehicle later, you'll need to convert to a standard SR-22 policy covering that specific vehicle. The filing period doesn't restart when you convert, but the new policy premium will be higher because it includes comprehensive and collision options.

What Happens If the Owner's Insurance Should Have Covered You

Some borrowed-car accidents involve coverage disputes. The owner claims they gave you permission and their policy should cover permissive use, but the carrier denies the claim citing an exclusion, a policy lapse, or lack of evidence you were an authorized driver. Your suspension proceeds regardless of the coverage dispute because the DMV bases suspension on the accident report showing no valid insurance at the scene.

You can challenge the suspension if the owner's policy definitively covered you. This requires obtaining a copy of the owner's policy declarations page, proof of permissive use (written permission, text messages, or the owner's signed affidavit), and the carrier's claim file showing coverage applied at the time of the accident. Most states allow a 10 to 30-day administrative appeal window from the suspension notice date. Missing that window forfeits your appeal and the suspension becomes final.

Even if the appeal succeeds and the suspension lifts, the SR-22 requirement may remain if the state cited you for an uninsured-driving violation at the scene. The ticket and the suspension are separate enforcement actions. The ticket creates a court obligation with fines and points; the suspension creates a DMV reinstatement requirement. Resolving one doesn't automatically resolve the other.

Borrowed-Car Accidents and Hardship License Eligibility

Hardship license eligibility after a borrowed-car accident depends on how your state classifies the violation. States treat uninsured-driving violations inconsistently. Some categorize them as insurance-compliance failures eligible for hardship driving; others classify them as moving violations or financial-responsibility violations ineligible for restricted driving privileges.

New Jersey, Pennsylvania, and Washington prohibit hardship licenses for uninsured-driving suspensions entirely. If your suspension originated in one of those states, your only option is full reinstatement: SR-22 filing, fee payment, and waiting out the suspension period. Other states allow hardship applications but restrict approved purposes to employment, medical appointments, education, and court-ordered obligations. Recreational driving, errands, and social trips remain prohibited during the hardship period.

Hardship applications require documentation. Employers must submit affidavits confirming your work schedule, start time, and job-site address. Medical providers must document ongoing treatment requiring your attendance. The court or DMV reviews your application and approves specific routes and time windows—typically 12 hours per week for work, plus 2 to 4 hours monthly for medical or court obligations. Violating those restrictions triggers automatic hardship revocation and extends your full suspension period.

Cost Breakdown: Accident Settlement, Reinstatement Fees, and SR-22 Filing

The total cost of a borrowed-car uninsured accident includes the accident settlement, your license reinstatement, and ongoing SR-22 premiums. Accident settlements vary by damage severity. Minor property-damage-only crashes settle for $2,000 to $8,000 if the other vehicle sustained moderate damage. Injury claims escalate quickly—medical bills, lost wages, and pain-and-suffering demands push settlements into the $15,000 to $50,000 range for serious injuries.

Reinstatement fees for uninsured-driving suspensions range $100 to $500 depending on state and violation tier. First-offense violations fall on the lower end; repeat violations or accidents involving injury increase the fee. Some states add separate accident-responsibility fees if the crash caused property damage above a statutory threshold—typically $1,000 to $2,500 in total damage.

SR-22 insurance premiums over a 3-year filing period add $1,500 to $3,200 in total cost for non-owner policies, more for standard policies covering an owned vehicle. This stacks on top of the reinstatement fee and any settlement or judgment from the accident claim. Drivers who can't afford the upfront settlement often negotiate payment plans with the other driver's carrier or face wage garnishment when the carrier obtains a judgment.

What to Do Right Now: Securing Coverage and Protecting Your License

Start by confirming your suspension status. Contact your state DMV or check online license status using your driver's license number. The suspension notice lists your effective suspension date, required reinstatement steps, and filing period duration. If you haven't received the notice yet but the accident report documented no insurance, expect suspension within 10 to 30 days.

Secure SR-22 coverage immediately. Contact non-standard or high-risk auto carriers—Progressive, The General, Bristol West, Acceptance, National General—and request a non-owner SR-22 quote if you don't currently own a vehicle. If you do own a car, request a standard SR-22 policy. The carrier files the SR-22 certificate electronically with your state DMV within 24 to 72 hours of policy activation. Confirm the filing with the DMV 5 to 7 business days later to ensure it posted correctly.

Address the accident claim separately. If the other driver's carrier contacted you, respond within the timeframe stated in their demand letter—typically 30 days. Ignoring the claim leads to default judgments and extended suspension in states that tie license reinstatement to financial responsibility judgments. If you can't afford the settlement, ask about payment plans or consult a consumer attorney about negotiating a reduced settlement amount.